Money makes the world go round.

If you’re running a business, there’s a good chance that you’ll need to borrow money to support the company at some point.

However, with the amount of paperwork required to take out a loan, it can quickly become a challenge to keep track of what you owe and who to. That’s where notes payable can help you out.

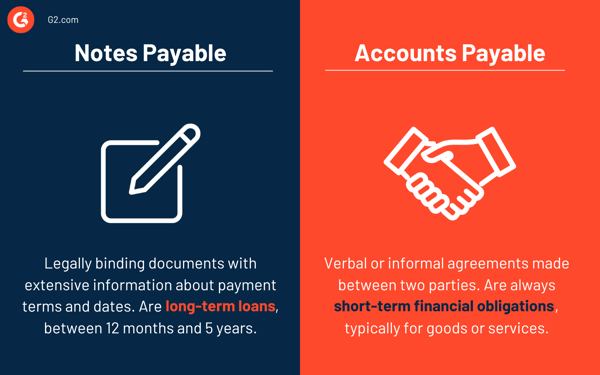

Notes payable are a type of promissory note or formal IOU between a borrower and a lender. They’re written agreements that outline the details of a loan from one party to another. They typically include information like the amount paid, the interest rate on the loan, the maturity date, the names of both parties, and the signature of the borrower.

All notes payable should be entered into a business’s accounting software to keep a record of what’s still left to pay on the loan and the recurring payments that are being made. Accounts payable automation software is one of the best ways to do this, keeping track of large volumes of financial transactions between businesses.

Although most often used by businesses for loans between the business and a bank or a vendor, notes payable can be used for any lending agreement. Other promissory notes can be used for transactions like car loans, student loans, or other non-commercial lending. On the lender’s end, incoming funds from the notes payable agreement are known as notes receivable.

Both notes payable and accounts payable are frequently used interchangeably, but it’s important to understand the difference between them, especially when looking at a business balance sheet.

Notes payable are considered to be long-term loans over 12 months but usually less than 5 years. The borrower, or maker of the note, will create a liability with the lender for the amount they owe. It’s a specific amount that should decrease over time as the borrower pays back the lender for both the principal and interest amounts.

Accounts payable, though, are always short-term financial obligations, usually for goods or services. They don’t need a promissory note as they’re typically paid within a month. Utilities for the business, like electricity, water, heating, or goods provided by a vendor and invoiced to the business, are examples of line items that fall under accounts payable.

As accounts payable are typically for smaller amounts, these are verbal or informal agreements made between the two parties. Notes payable, like other promissory notes, are legally binding documents with extensive information about payment terms and due dates for the repayment of borrowed funds.

As a type of promissory note, notes payable are often used for big ticket items. They are large, long-term loans used in many industries, especially when heavy equipment, real estate, or supplies are being purchased. They may be issued when:

Short-term financial obligations are listed separately on a balance sheet under accounts payable. This could include:

There are several types of notes payable that a business could use, varying by the terms of the note, interest rates, and the amount owed. There are four commonly used types of notes payable.

With these notes, the total amount borrowed is due back to the lender in a single lump sum payment. Both the principal and interest are owed at the same time in one payment on the due date specified on the note.

Amortized notes are generally used for larger sums of money, as they set a sum that must be paid each month until the loan is fully repaid or the term expires. The amount due each month is the same, with some going towards the principal and some towards interest. As the amount on the loan decreases, more will go towards the principal. Real estate loans are the most common use for this type of notes payable.

These are somewhat the opposite of amortized notes, where payments are structured to be lower than they would be under a traditional loan to help the borrower afford the repayments. Any interest not paid each month is added to the principal balance, which means borrowers can end up owing more by the loan maturity date.

The only payments made during the course of the loan under this type of note are for the interest, not the principal amount. At the end of the loan, the total principal amount is then owed as a single lump sum. More interest will be paid on these loans as the interest amount will be calculated against the total principal amount for the lifetime of the loan, not getting smaller as the principal amount decreases.

As with most formal loans, notes payable amounts will include the actual amount of money borrowed and the interest owed on the loan. This means that more money will be paid by the end of the loan than simply the borrowed amount.

To calculate the total amount owed to the lender, borrowers can use the following calculation:

Notes payable = Amount of the loan x ( 1 + interest rate x number of payments)

For example, a $20,000 loan at an interest rate of 10%, with 60 total monthly payments, would be:

$20,000 x (1 + 0.1 x 60) = $140,000

This information should all be recorded on a business’s balance sheet to determine how much of the loan amount still needs to be repaid and to ensure that payments are being completed according to the schedule outlined in the notes payable documents.

Keeping business books organized with notes payable information is essential for maintaining good financial records, especially if your company has multiple notes with different lenders.

Whether you have one large loan or several smaller ones, notes payable hold each party accountable for their accounts!

Understand the comings and goings of your business finances with cash flow management services that help you stay on top of loans and forecast future revenue.

Keeping tabs on what you owe to different lenders can be challenging as a business owner, but with notes and accounts payable automation tools, your finances are always up-to-date.

Debt can be scary when you’re paying off college loans or deciding whether to use credit to...

by Maddie Rehayem

by Maddie Rehayem

Regardless of a company's size, the accounts payable (AP) department fulfills an essential...

by Kayla Matthews

by Kayla Matthews

Supplier crossovers are the new business order.

by Adam Miller

by Adam Miller